With financial experts insisting that you’ll need about 75% to 85% of your pre-retirement income to retire comfortably, it’s understandable why Americans are increasingly looking to diversify beyond the traditional retirement investment options and retirement accounts.

In particular, it turns out that cryptocurrencies are fast becoming a favorite alternative for many young Americans. So much so, in fact, that nearly 50% of US Millenials and Gen Z-ers today are reportedly already planning to include them in their retirement investment plans.

It just so happens, however, that while federal laws allow you to pursue such investments, there are special rules and provisions for investing in cryptocurrency in your retirement account. This is where crypto IRAs (often marketed as a “Bitcoin IRA” as bitcoin is the most popular cryptocurrency) come in to provide a legal means of earmarking cryptocurrency as part of your retirement savings.

The following is a simplified breakdown of what crypto IRAs entail, how they operate, what to expect from them, plus how and where to open such accounts.

Table of Contents

What is a Crypto IRA?

Crypto IRA is a special type of self directed account that gives you the power to purchase, hold, and invest in cryptocurrencies such as bitcoin or ethereum as part of your tax exempted retirement plan.

IRA, in this case, stands for Individual Retirement Account. Think of it as the blanket term for long-term retirement savings accounts that allow you to invest in various types of assets. You get to grow your retirement income while, at the same time, enjoying the tax benefits attached to the accounts.

It’s worth noting, however, that the structure of the IRAs is not uniform across the board. They come in different categories and subcategories, with each operating under its own set of rules and privileges.

At the top, for instance, we have regular IRAs and self-directed IRAs.

Regular ones are the standard retirement savings accounts that are offered by banks, investment companies, and brokerage firms. If you have a 401k through your employer, that is a standard retirement account.

You essentially deposit pre-tax or after-tax dollars, which are then channeled into mainstream investment securities such as stocks, exchange-traded funds (ETFs), bonds, and certificates of deposit (CDs). This entire portfolio is then managed by your retail brokerage firm in exchange for a commission or flat fee. Transaction fees are low but alternative investments like metals or bitcoin are not possible.

Self-directed IRAs (SDIRAs), under which crypto IRAs fall, are conversely managed by the account holders themselves. They are reserved for unconventional investment assets like real estate, tax lien certificates, limited partnerships, private placements, cryptocurrencies, commodities, and precious metals.

That said, both SDIRAs and regular IRAs have subcategories of accounts that offer varying tax benefits, deduction limits, funds management procedures, and contribution limits.

You could, for example, choose to register your account as a Traditional crypto IRA. Traditional IRA’s allow you to contribute pre tax income, acquire digital assets like Bitcoin, trade or hold them and let you defer the taxes on capital gains through the entire investment period. Bitcoin IRAs only owe taxes on the gains when you withdraw the funds.

Roth crypto IRAs, on the other hand, have their tax benefits applying the other way around. You put in money you earned and already paid taxes on (say from your paycheck) and can trade or hold crypto without paying any capital gains taxes on the withdrawal. The tax advantages of ROTH ira’s make them more popular for many Bitcoin IRA companies.

How it works

Unlike regular IRAs, Bitcoin IRAs are held by a distinct category of SDIRA providers who specialize in cryptocurrencies. They are known as custodians, and their only job is to administer cryptocurrency IRA accounts while maintaining compliance with IRS regulations.

That means you won’t be getting any help with the management of your cryptocurrency portfolio. What’s more, such custodians are not even allowed to offer their clients any form of investment advice. You need to be confident in your skills and ability to trade and invest in digital assets.

Many of them are primarily registered as credit unions, banks, or investment firms that double up as trustees of cryptocurrency IRAs.

They don’t work alone, though. The setting up and running of Bitcoin IRAs is an intricately complex process that requires the joint effort of three principal modules. You’ll need:

- A custodian to host and administer the retirement account. This is where you place the banks and firms that are entrusted with the opening and safekeeping of the crypto IRAs. They are the ones who report directly to the Internal Revenue Service (IRS), all the while ensuring that your account remains fully compliant with federal directives.

- An exchange to facilitate the trading of cryptocurrency. It operates more or less like a typical stock market, allowing you to purchase and sell different types of digital currencies.

- A crypto wallet to securely hold all the cryptocurrencies in your portfolio. You can think of it as the safehouse or vault that protects your hard-earned Bitcoin, Ethereum, or any other crypto.

Some of the leading self-directed IRA providers today happen to provide all three elements under one all-inclusive platform. You’ll find, for instance, account custodians who’ve linked up with third-party trading marketplaces and crypto storage solutions.

Why Use a Crypto IRA

Portfolio diversification

Whereas all forms of investment accounts contribute to portfolio diversification, not many are as uncorrelated as bitcoin IRAs.

You see, with this type of account, you get to that stretch your investment portfolio beyond even the standard market parameters.

The cryptocurrencies that you’ll be adding are built on a decentralized blockchain, which is free from all forms of jurisdiction, government control, and geographical restrictions. That means you’ll have at least one asset running independently of all the market variables that may affect the rest of the investments in your retirement accounts.

This could be your lifeline if a repeat of the 2008 financial crisis ever happened. While your retirement account may suffer as stocks, ETFs, bonds, and other mainstream assets succumb to a market crash, bitcoin held in your self directed IRA may do well in a market crash.

High ROI potential

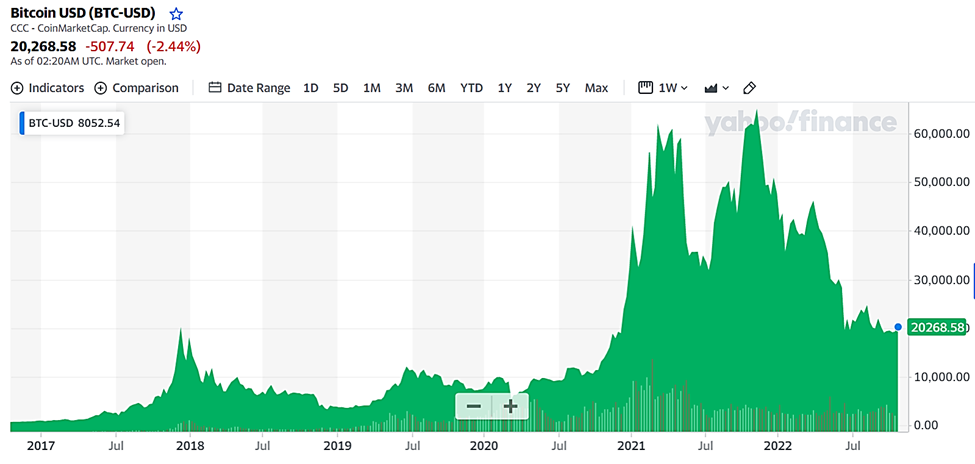

Although cryptocurrencies are widely criticized for their volatility, charts show that it’s the same volatility that could ultimately rewards long-term investors with a high ROI.

Consider, for instance, Bitcoin, which now ranks as one of the most volatile investments you could have in your IRA account.

Short-term speculators have had a rough year so far, as the cryptocurrency has dropped from 2021’s all-time high of $60,000 to its current value of $20,000.

Interestingly, however, their downturn is a stark contrast to the returns that crypto IRA investors are generating from their long-term Bitcoin investments. The ones who invested their money in 2017, for example, are now twenty-fold richer – despite Bitcoin’s recent decline.

Bitcoin price chart. Source: Yahoo Finance

As such, you could say that by giving you chance to play long ball, crypto IRAs tend to have a higher risk tolerance than short-term crypto investment options.

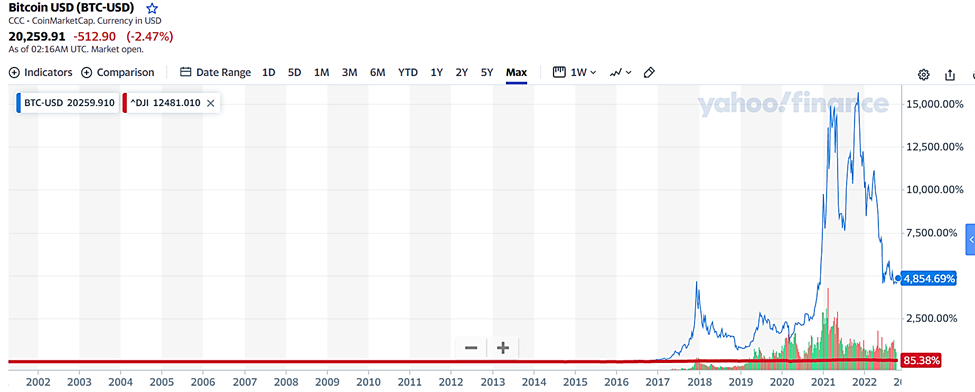

And that’s not all. If you, otherwise, compared Bitcoin’s run with the Dow Jones’, you’d notice that crypto IRAs tend to outshine even popular “stable” assets in long-term ROI. The DJIA, which is the less volatile option, has only seen an 85% growth in value since 2005 – while Bitcoin has grown by over 4,800% in just five years.

Bitcoin vs Dow Jones. Source: Yahoo Finance

Tax benefits

In 2014, the IRS ruled that cryptocurrency would, henceforth, be categorized as a capital asset instead of a currency. This has since complicated things for crypto owners, as they’re now required to file all positive changes in value as taxable capital gains.

Imagine, for instance, you acquired $80 worth of Bitcoin and then held on to it until the value appreciated to say $400. If you went on to use it to buy stuff worth $400, the IRS would still treat the $320 difference as a taxable capital gain.

Keeping track of all these tax obligations is, of course, no mean feat. It can be pretty overwhelming for not only high-volume cryptocurrency traders, but also long-term holders with a relatively low volume of transactions.

Now, to save themselves all that trouble and the legal ramifications that come with it, cryptocurrency investors are now turning to crypto IRAs. This allows them to hold on to all forms of recognized cryptocurrencies without worrying about tax liabilities.

This is courtesy of the leniency the IRS famously accords retirement savings accounts, as it extends tax benefits to both Traditional and Roth crypto IRAs.

In the case of Traditional crypto IRAs, for example, contributions are treated as tax deductible. That means you can exclude them from your income tax bill, up until you finally make a withdrawal. It’s only when you start enjoying the returns you’ll be required to remit the deferred income tax.

With Roth crypto IRAs, however, taxes are only levied at the beginning. You’re supposed to count your contributions as taxable income, after which you get to keep every dollar made from the investment account. That means the IRS won’t be expecting any tax remittances from your withdrawals.

How to Open a Crypto Roth IRA

If you choose to invest in a crypto Roth IRA, one of your very first stops should be a self-directed IRA custodian. You need to find an SDIRA company that supports crypto Roth investments and then register an account with them.

Keep in mind, however, that the companies here don’t necessarily operate in the same way. You’ll come across banks and investment institutions that administrate their crypto Roth IRAs under different policies, procedures, charges, and provisions.

The only commonality between them is the federal regulations governing their investment accounts. Every SDIRA custodian is, for instance, required to open an account with your full legal name, social security number, address, and banking information. So, you might want to collate all the valid identification documents beforehand.

Otherwise, when it comes to picking a custodian, we’d advise you not to rush it. You should, instead, take the time to research widely and compare the offerings from various providers. Only then will be able to confirm the SDIRA custodian that perfectly fits your budget and investment goals.

With that said, two prominent examples of crypto Roth IRA administrators are:

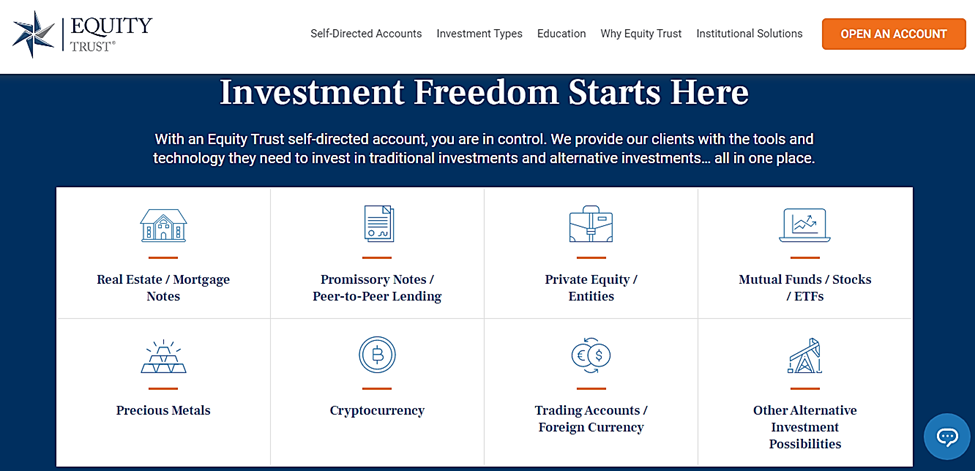

Equity Trust

Boasting a portfolio of over $34 billion under its administration, Equity Trust is an SDIRA custodian that gives you the tools and technologies to invest your retirement savings in cryptocurrency, real estate, promissory notes, private equity, precious metals, mutual funds, ETFs, and stocks.

Opening an account here will cost you a $50 setup fee, after which the company will proceed to levy an annual administration charge of between $74 and $2,640, plus a monthly cold storage fee of 0.07% on the value of your crypto investments.

All this while, you should be able to put your retirement savings into Bitcoin, Litecoin, Ethereum, Bitcoin Cash, Ethereum Classic, Zcash, Stellar Lumen, and Chainlink.

Bitcoin IRA

Just like Equity Trust, Bitcoin IRA serves not only as a crypto Roth IRA custodian, but also as a trading service and cold storage provider.

Don’t be misled by its name, though. Bitcoin IRA isn’t restricted to Bitcoin. Rather, it grants you access to over 60 other cryptocurrencies – including Litecoin, Cardano, and Ethereum.

You should be able to open your account via Bitcoin IRA’s website or app. The process itself takes a couple of minutes, during which you’ll be required to pay a $50 account setup fee.

Then when you finally start trading, you can expect to incur an annual account maintenance charge of $195, along with an offline storage fee of 0.05% per month.

Over to You

Other renowned Roth crypto IRA companies include;

- Regal Assets

- iTrustCapital

- Bit IRA

- Coin IRA

To make an informed choice, you can check out their customer reviews on acclaimed business accreditation platforms like Better Business Bureau. You might want to particularly pay attention to the comments left by long-term crypto investors.

And while you’re at it, consider enrolling in a training program for crypto investors. You’ll need all the investment skills and knowledge you can get to strategically manage your crypto IRAs. Remember that the account custodians won’t do it on your behalf.